In this episode, Denise Herman, Inpatient DRG Validator & Coding Analyst at BESLER, shares peak into BESLER’s upcoming Webinar, Coding Clinic Q1 2025: Key Updates & Guidance, live on July 9, at 1 PM ET.

SUBSCRIBE for Weekly Insider Updates

In this episode, Denise Herman, Inpatient DRG Validator & Coding Analyst at BESLER, shares peak into BESLER’s upcoming Webinar, Coding Clinic Q1 2025: Key Updates & Guidance, live on July 9, at 1 PM ET.

Access the latest healthcare finance news and BESLER news from the week of June 23, 2025.

Watch BESLER Webinar–NJ DSH Survey 2022. Gain a deeper understanding of the key metrics that influence reporting and the potential financial impact of your submission. .

In this episode, Dr. Terrance Govender, VP of Medical Affairs at ClinIntell, discusses solving the physician engagement puzzle & why it matters for hospital finance.

Access the latest healthcare finance news and BESLER news from the week of June 16, 2025.

BESLER’s SVP of Growth, Randi Deckard, moderates an insightful discussion with Jeff Davis, Partner at Bass, Berry & Sims, & Christina Brown, BESLER’s VP of Reimbursement. They explore the critical connection between reimbursement strategies & 340B.

In this episode, Erik Swanson, Managing Director leading Kaufman Hall’s Data & Analytics Group, discusses the latest Kaufman Hall Hospital Flash Report with data through April 2025.

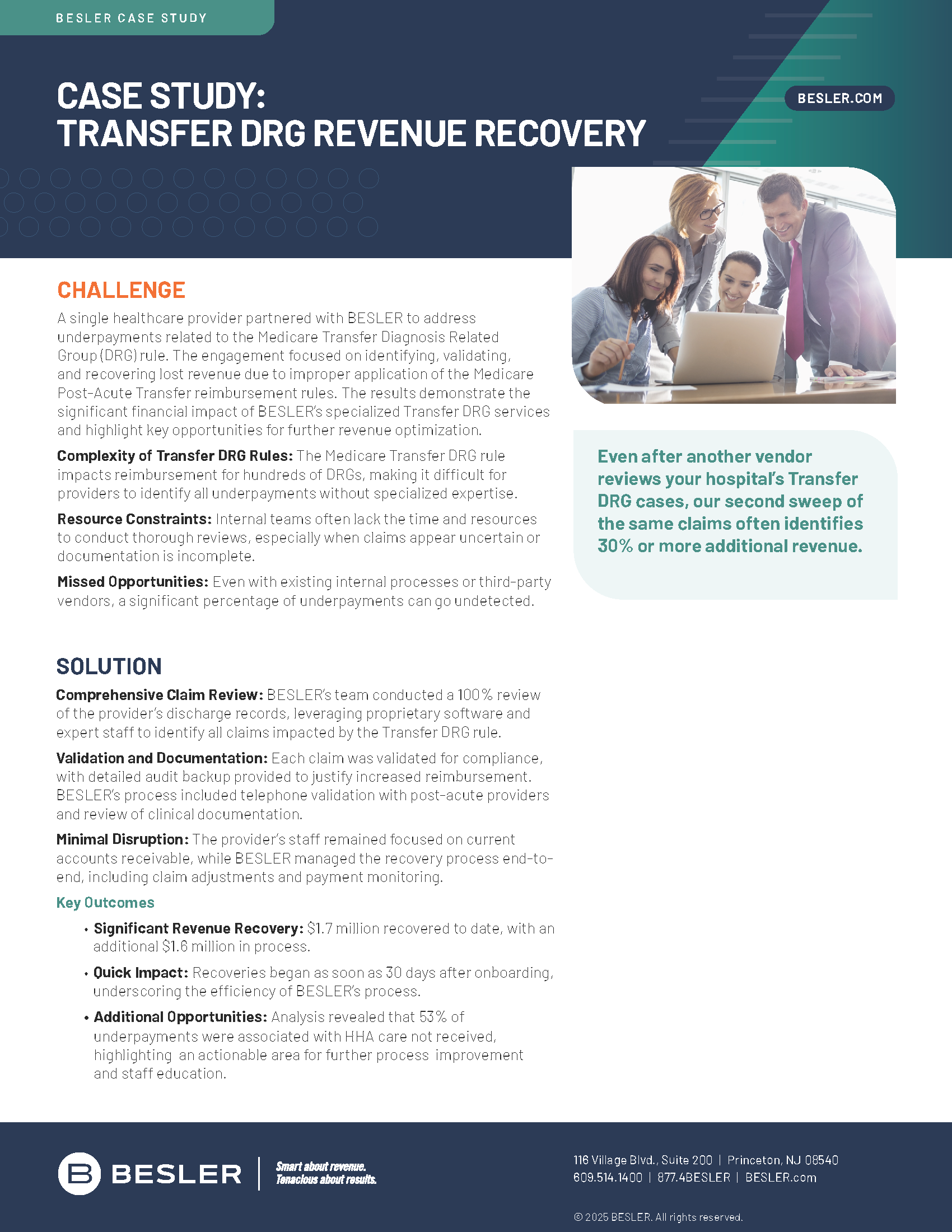

BESLER’s Transfer DRG solution helped a hospital address underpayments related to the DRG rule resulting in significant revenue recovery. Read this Case Study.

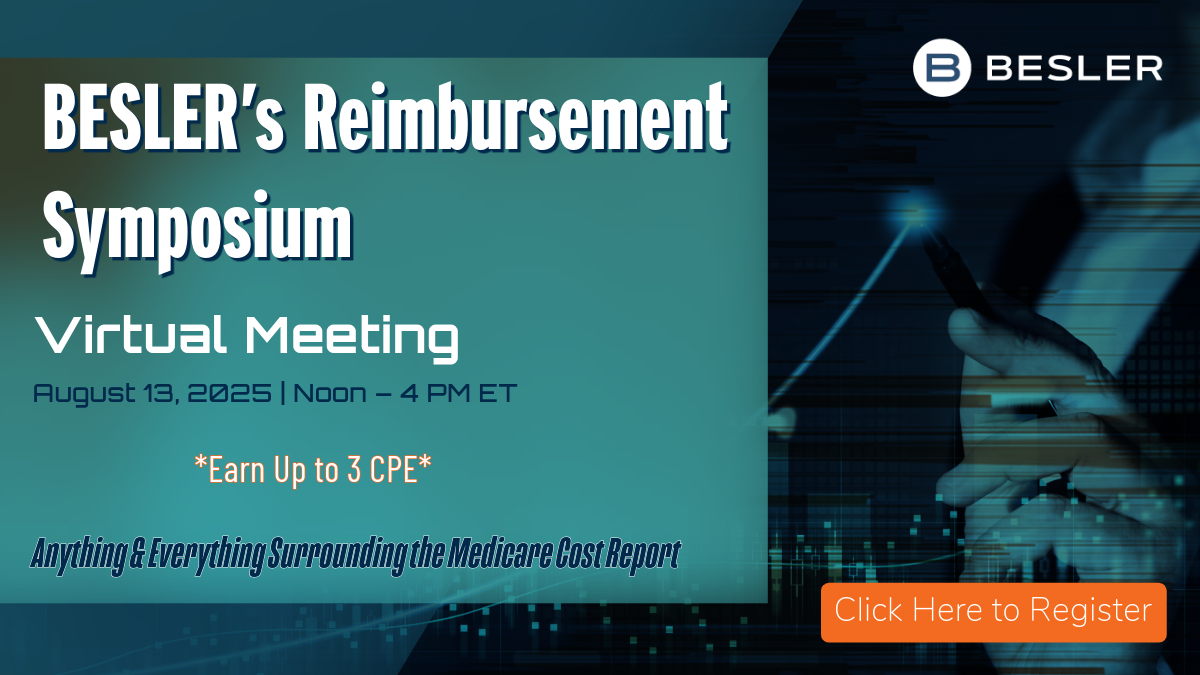

BESLER’s Reimbursement Symposium is scheduled for August 13, 2025, Noon – 4 PM ET. Earn CPE. Save the date & register today to join us.

Access the latest healthcare finance news and BESLER news from the week of June 9, 2025.

SUBSCRIBE for Weekly Insider Updates

By submitting your email address, you are agreeing to receive email communications from BESLER.

BESLER respects your privacy and will never sell or distribute your contact information as detailed in our Privacy Policy.